Sovereign strains also spilled into the euro zone banking

system as some funding channels closed, and interbank

spreads widened. Banks’ access to term funding was sharply

curtailed and even short-term markets came under strain as

lending tenors were reduced from months and weeks to days.

U.S. money market funds dramatically scaled back credit to

euro area banks (Figure 2).

This prompted many of those banks to sell U.S. dollar

assets. In many markets, the cost of funding now exceeds

that during the Lehman crisis. Funding strains are beginning

to spill over into the broader economy with tighter

conditions for accessing bank credit for small and

mediumsized enterprises and households as banks' ability to

fund assets diminishes, leading to rising credit risk

(Figure 3).1

The potential impacts of funding strains are already

evident. A number of banks have announced significant

balance sheet deleveraging plans. These plans include

shedding assets in the euro area, the United States, and

other developed markets, as well as in the emerging

economies. The execution of some of these plans by affected

banks could impact a wide range of economic activities, from

trade and project finance, to cross-border arbitrage.

European policymakers have taken significant

steps to contain the crisis . . .

EU summit meetings in October and December led to

agreements on important steps to stabilize market conditions

and restore confidence. The EU will work toward stronger

joint economic governance, and growth-enhancing structural

policies will be given greater weight. Banks are to be

strengthened with new capital and funding support. The Greek

debt overhang is to be addressed through a voluntary debt

exchange with private creditors. The European Financial

Stability Facility (EFSF) is to be enhanced to help banks

and finance national adjustment programs, and the starting

date for the European Stability Mechanism (ESM) is to be

brought forward to July 2012.

. . . while the outlook for sovereign risk in

some larger economies has worsened.

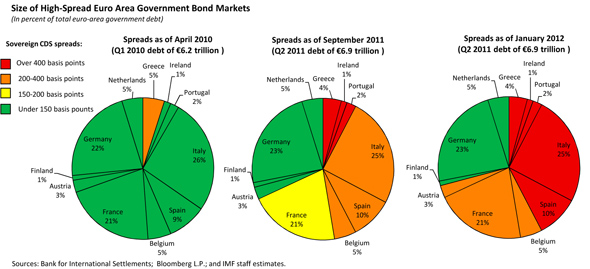

Negative sovereign ratings actions have spread beyond

Greece, Ireland, and Portugal further into other euro area

countries (Figure 3). This reflects concerns that it will be

difficult to reach the political consensus necessary for

fiscal consolidation and structural reforms. Market concerns

are also rising about the fiscal path in the United States,

given little evident progress in breaking the political

stalemate over how to carry out needed fiscal consolidation.

In the near term, markets have focused on a potential

failure to raise the debt ceiling, which the U.S.

authorities have estimated will become binding at the

beginning of August, absent action. The risk of a temporary

default has pushed U.S. short-term CDS spreads above those

of some countries rated below the United States’s AAA

rating. Even that rating has come under question following

S&P’s issuance of a negative outlook in April. In Japan,

ratings agencies have downgraded the sovereign outlook on

concerns about the government’s ability to achieve deficit

reduction.

National governments have recently taken important steps

to improve macro-financial stability. Following changes in

government, Italy and Spain both announced measures to cut

structural budget deficits, improve debt-to-GDP ratios over

the medium term, and address longstanding structural

rigidities in order to enhance growth prospects.

With private funding markets for euro area banks under

severe strain, including due to a lack of eligible

collateral to conduct repo operations, the ECB took

extraordinary steps to stabilize funding conditions.

Measures included cutting reserve requirements, broadening

eligible collateral, and offering 3-year longer-term

refinancing operations (LTROs) to mitigate the effects of

funding stress on credit provision to the private sector,

and provide an alternative to forced fire sales of assets.

To alleviate dollar funding strains, the U.S. Federal

Reserve and five other central banks reduced the cost of the

existing dollar swap lines. While market functioning remains

far from normal, several of these measures – most notably

the 3-year LTRO – have had positive effects on market

sentiment and funding conditions.

. . . but stability risks remain elevated as

sovereign financing will be challenging and backstops are

not yet adequate . . .

Restoring sovereign access to funding at sustainable

yields is a key challenge as many remain vulnerable to

shifts in market sentiment. However, regaining market

confidence is likely to take time, during which domestic

reform may need to be supplemented by short-term external

support for primary or secondary markets, if available

support from private markets is insufficient. While the

3-year LTRO did much to alleviate bank funding concerns,

thus far it has had less of an impact on peripheral

sovereign yields, which, while declining at the short end of

the yield curve, were little changed at the long end.

The EFSF can now operate in primary and secondary public

debt markets, but its capacity remains limited. Taking into

account resources already committed to program financing, it

only has about €300 billion available to deploy. While some

proposals to leverage the EFSF have merit, even with a

plausible amount of leverage the total amount of firepower

available would still likely not be sufficient to contain

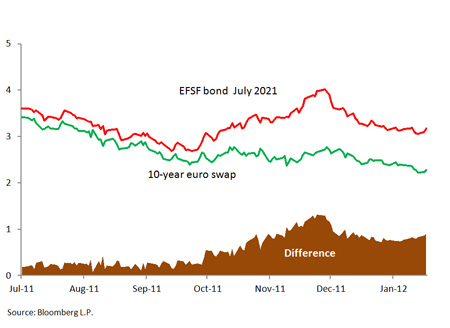

rising sovereign spreads under stress scenarios. Moreover,

the recent widening in EFSF spreads (Figure 4) and S&P’s

decision to downgrade the facility’s AAA rating in

mid-January suggest that even the current funding model for

the facility may be under pressure.

. . . and deleveraging by banks may ignite an

adverse feedback loop to euro area economies . . .

Pressures on European banks have recently escalated,

reflecting the increase in sovereign stress and the closure

of many private funding channels. To insulate banks from

such negative shocks, global steps toward a safer financial

system are essential. In this regard, the European Banking

Authority (EBA) has initiated a process calling for banks to

reach higher capital ratios.2

It judged €85 billion in additional capital to be necessary

(excluding €30 billion already programmed for Greece) to

reach a 9 percent core Tier 1 ratio and provide an adequate

sovereign capital buffer (Figure 5).

There remains the potential for an adverse feedback loop

between credit markets and the real economy in the euro area

and beyond, as outlined in the downside scenario described

in the

January 2012 World Economic Outlook Update. The ECB’s

recent actions likely forestalled an imminent crisis as

substantial debt maturities need to be rolled over this year

by euro area banks, with large amounts due in the first

quarter. But even with this funding and a subsequent LTRO to

be conducted in February, deleveraging could still be

substantial.

While some deleveraging may be unavoidable, the way it is

done makes a difference—there is "good" and "bad"

deleveraging. Some types of balance sheet deleveraging do

not necessarily represent a reduction in credit to the real

economy. For example, some banks (especially in Germany,

Ireland, and the United Kingdom) are seeking to reduce

balance sheets by shedding some assets that remain on

balance sheets as a legacy of the original leg of the credit

crisis. In other cases, banks may sell non-core businesses

(e.g., asset management arms, insurance business, or

overseas operations) or even loan portfolios. In cases where

this results in a transfer of assets to strong hands, it

would not reduce credit to the economy, although asset sales

can cause declines in asset prices whose adverse impact goes

far beyond the sellers, further pressuring capital. However,

provision of credit to the real economy is most affected

when banks decide to let credit lines and loans run off and

curtail new loan originations.

. . . that could exacerbate financial stability

risks in the United States . . .

The U.S. economy is susceptible to a range of shocks from

the euro area, reflecting the close financial and trade

integration extending across the Atlantic. Potential

spillovers could include direct exposures of U.S. banks to

euro area banks or the sale of U.S. assets by European

banks. For example, the CMBS and ABS markets have been under

pressure in recent months, weighed down by the volume of

European asset sales. Funding strains more generally could

rise, transmitting pressure to the U.S. banking system. An

important demonstration of this is the persistent widening

of interbank spreads in dollar markets since mid-2011, in

parallel with the widening of euro interbank spreads.

Some domestic risks also remain. While U.S. sovereign

financing conditions have generally benefited from a flight

to safety away from the euro area, such a situation cannot

be counted on to persist indefinitely. It is thus necessary

to resolve the political impasse over the fiscal situation

in the United States, as noted in the January 2012 WEO

Update. While the U.S. banking system has regained a good

measure of health since the crisis and ongoing Federal

Reserve stress tests should continue to enhance

transparency, legacy problems in the mortgage sector remain,

weighing on consumption, and pushing some of the burden of

sustaining demand onto the public sector. More broadly,

banks will struggle to maintain historical returns on

equity, particularly in a new, tighter regulatory

environment.

. . . threaten emerging Europe and spill over to

emerging markets more broadly.

Emerging Europe would be heavily affected by deleveraging

on the order of that assumed in the downside scenario

described in the

January 2012 WEO Update, reflecting the large

presence of euro area banks in those economies. The deep

recession in emerging Europe in 2009 was largely the result

of the sudden stop in capital flows from western European

banks, which abruptly ended the credit boom.

Emerging markets beyond central and eastern Europe could

face spillovers from the European debt crisis through

several channels. Overall macroeconomic prospects

for emerging markets have already deteriorated, and are

subject to downside risks stemming from Europe, as discussed

in the

January 2012 WEO Update.

While emerging markets outside of Europe have been quite

resilient to shocks and developments in major economies in

the past year, recent indicators have weakened significantly

and the general business climate has deteriorated.

First, credit channels could become impaired as

pressures on European banks result in a pullback of

cross-border lending, notably trade finance activities, and

a loss of parent bank support for local lending. For

example, euro area banks provide roughly 30 percent of trade

and project finance in the Asian region, even though their

balance sheets account for only about 5 percent of bank

assets. The impact depends on the extent to which local

banks can step in and fill the financing gap: even though

some banks may have the balance sheet capacity to do so,

there are significant operational challenges in some areas

of trade finance. New entrants will also have to raise

substantial dollar funding in stressed market conditions.

Constraints on long-term funding could severely limit banks’

capacity in such areas as shipping and aviation trade

finance, as well as project and infrastructure finance.

Second, local asset markets (foreign exchange,

fixed income, and equity markets) could come under renewed

strains through outflows, deteriorating liquidity, and a

repricing that could have a knock-on impact on local

financing conditions. Emerging markets that are heavily

reliant on external portfolio flows could be especially

susceptible.

How resilient are emerging markets in the face of these

challenges? Many emerging markets have built up considerable

capital and liquidity buffers to counter adverse shocks, and

local markets generally held up well under the strains of

the Lehman crisis. Since then, some have built up further

(albeit limited) headroom to conduct countercyclical

economic policies, although the situation varies across

regions and countries. Emerging Europe is particularly

vulnerable, in view of the concentration of European bank

lending and the dependence on Europe as an export market. In

that region, buffers are generally weak relative to other

emerging market regions, and other longstanding

vulnerabilities in the financial system, including maturity

and currency mismatches in some economies, could strain

balance sheets.

Additional policy actions are needed for a

comprehensive plan.

Faced with the above risks, policymakers in all major

economies need to focus on a number of interlocking

challenges. European policymakers need to promptly put in

place a comprehensive package that restores confidence. In

addition to pursuit of appropriate macroeconomic and

financial policies, European policymakers need to implement

vigorously the policy measures agreed at the October and

December summits.

Furthermore, there is a need to: provide a sufficiently high

firewall that avoids a destabilizing spiral of high funding

costs for sovereigns and banks; manage the process of

balance sheet adjustment in the banking system to prevent a

disorderly deleveraging and, instead, promote an adequate

flow of credit to the private sector; and take additional

measures that may be necessary to bolster confidence in the

global financial system, for both emerging and advanced

economies. Achievement of this policy agenda will require

prompt and thorough implementation of recent initiatives,

and the adoption of new policies to promote and enhance

financial stability.

In particular:

- The "firewall" needs to be sufficiently large

and convincingly built. Sovereigns that are solvent

but facing financing strains may require an extended

period of successful policy implementation before

investors return. During the intervening period, it is

crucial to secure affordable funding from external

sources. The EFSF was meant for this purpose in the euro

area. However, given its size and structure, the EFSF

has a limited ability to undertake this role. To

establish confidence, it would be highly desirable to

increase the size and flexibility of the EFSF/ESM at the

earliest possible opportunity. Until this larger

firewall is wellestablished, provision by the ECB of

substantial and sustained liquidity support to stabilize

government debt and bank funding markets remains

essential.

- A "macroprudential gatekeeper" is needed to

assure deleveraging plans are consistent with sustaining

the flow of credit to support economic activity and

to avoid a downward spiral in asset prices. Within the

EU, such a role could be coordinated among the EBA,

European Systemic Risk Board (ESRB), the national bank

supervisors, and the banks themselves. Countries should

aim to monitor and limit deleveraging of their banks not

only in home markets but also abroad, where such efforts

would normally take place in cooperation with host

country regulators. A potential precedent for such a

gatekeeping function is the current Vienna Initiative,

which aims to coordinate national efforts to avoid

adverse cross-border effects on emerging Europe

associated with deleveraging on the part of euro area

banks.

- A credible increase in banks’ capital buffers

along the lines recommended by the EBA remains necessary

to restore market confidence. As envisaged in the

EBA guidelines this should be done as far as possible by

increasing capital rather than reducing credit. Steps

are already being taken to require banks to meet a

certain level of nominal capital (as was the case under

the Troubled Asset Relief Program in the United States

and the Fund for Orderly Bank Restructuring in Spain)

rather than a ratio, which provides incentives to shrink

assets. Banks should be encouraged to raise capital from

private sources. However, given some recent challenges

for banks in doing so, public funding should be made

available as a backstop to such efforts, but should be

subject to strict conditionality. Some bank capital

could be raised via pari passu injections with the

government or via contingent capital instruments.

In addition, there needs to be a pan-euro-area facility

with the capacity to take direct stakes in banks. To

complement the ECB’s LTRO, bank guarantee schemes should

be established at the euro area level to help reopen

private funding markets. Finally, a weak tail of banks

with low capital, poor profitability, and vulnerability

to funding shocks still exists, acting as a drag on

recovery. Some of these will need to be restructured and

recapitalized, or resolved.

- Adjustment remains essential, but the nearterm

impact on growth should be taken into account. As

recognized by policymakers, in most of the advanced

economies it is essential to make a credible commitment

to fiscal consolidation over the medium term, in order

to remove the long-term tail risk of sharp increases in

sovereign spreads. However, the rhythm of fiscal

adjustment also needs to take into account the impact on

current economic conditions. As outlined in the January

2012 Fiscal Monitor Update, automatic stabilizers should

be allowed to operate in the event that growth slows

more than expected and in the United States, expiring

policies designed to support demand need to be renewed.

Monetary policy should also be sufficiently

accommodative and, when needed, structural policies

should be aimed at promoting growth, notably by

restoring the competitiveness of the private sector.

- Policymakers in emerging markets should stand

ready to counter funding and credit strains, and to

deploy countercyclical policies where headroom is

available. Emerging markets in many cases have

built ample cushions of reserves that could be used to

counter external liquidity shocks. An adequate and

flexible combination of macroeconomic and financial

policy measures can help limit the impact of external

shocks, but care should be taken to avoid generating

financial distortions.

1—

See Euro Area Bank

Lending Survey, ECB at

http://www.ecb.int/stats/money/surveys/lend/html/index.en.html.

2—The EBA issued a

recommendation on December 8, 2011 noting "Banks should

first use private sources of funding to strengthen their

capital position to meet the required target, including

retained earnings, reduced bonus payments, new issuances of

common equity and suitably strong contingent capital, and

other liability management measures. National supervisory

authorities may, following consultation with the EBA, agree

to the partial achievement of the target by the sales of

selected assets that do not lead to a reduced flow of

lending to the EU’s real economy but simply to a transfer of

contracts or business units to a third party."