Russian

Russian

World

Economic Outlook Update

Global Recovery Advances but Remains

Uneven

January 25,

2011

Download

PDF

The two-speed recovery continues. In advanced economies,

activity has moderated less than expected, but growth remains

subdued, unemployment is still high, and renewed stresses in the

euro area periphery are contributing to downside risks. In many

emerging economies, activity remains buoyant, inflation

pressures are emerging, and there are now some signs of

overheating, driven in part by strong capital inflows. Most

developing countries, particularly in sub-Saharan Africa, are

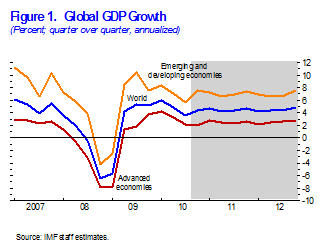

also growing strongly. Global output is projected to expand by

4½ percent in 2011 ( Table

1 and

Figure 1:

CSV| PDF) ,

an upward revision of about ¼ percentage point relative to the

October 2010 World Economic Outlook (WEO). This reflects

stronger-than-expected activity in the second half of 2010 as

well as new policy initiatives in the United States that will

boost activity this year. But downside risks to the recovery

remain elevated. The most urgent requirements for robust

recovery are comprehensive and rapid actions to overcome

sovereign and financial troubles in the euro area and policies

to redress fiscal imbalances and to repair and reform financial

systems in advanced economies more generally. These need to be

complemented with policies that keep overheating pressures in

check and facilitate external rebalancing in key emerging

economies.The global recovery is proceeding

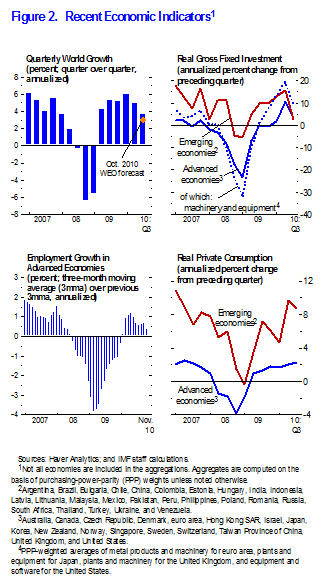

Global activity expanded at an annualized rate of just over

3½ percent in the third quarter of 2010. A slowdown from the 5

percent growth rate of the second quarter of 2010 was expected,

but the third-quarter rate was better than forecast in the

October 2010 WEO, owing to stronger-than-expected consumption in

the United States and Japan. Stimulus measures were partly

responsible for the strengthened outturn, especially in Japan.

More generally, signs are increasing that private consumption—which

fell sharply during the crisis—is starting to gain a foothold in

major advanced economies (Figure

2:

CSV|PDF).

Growth in emerging and developing economies remained robust in

the third quarter, buoyed by well-entrenched private demand,

still-accommodative policy stances, and resurgent capital

inflows.

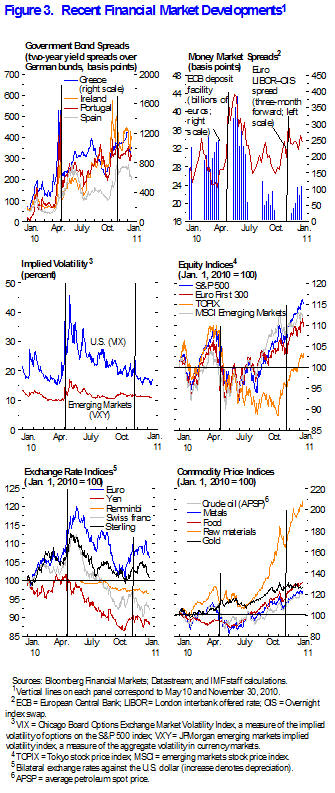

During the second half of 2010, global financial conditions

broadly improved, amid lingering vulnerabilities. Equity markets

rose, risk spreads continued to tighten, and bank lending

conditions in major advanced economies became less tight, even

for small and medium-sized firms. Nonetheless, pockets of

vulnerability persisted; real estate markets and household

income were still weak in some major advanced economies (for

example, United States), and securitization remained subdued.

And, in an echo of last May’s events, financial turbulence

reemerged in the periphery of the euro area in the last quarter

of 2010. Concerns about banking sector losses and fiscal

sustainability—triggered this time by the situation in Ireland—led

to widening spreads in these countries, in some cases reaching

highs not seen since the launch of the European Economic and

Monetary Union. Funding pressures also reappeared, although to a

lesser extent than during the summer. One key difference was

more limited financial market spillovers to other countries. The

turmoil in mid-2010 led to a spike in global risk aversion and a

scaling back of exposures in other regions, including emerging

markets. During the recent bout of turbulence, markets have been

more discriminating: measures of risk aversion have not risen,

equity markets in most regions have posted significant gains,

and financial stresses have been limited mostly to the periphery

of the euro area (Figure

3:

CSV|PDF).

|

Table 1. Overview of the World Economic Outlook

Projections

(Percent change, unless otherwise noted)

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Year over Year |

|

|

|

|

| |

|

|

|

|

|

Difference from October 2010 WEO

Projections |

|

Q4 over Q4 |

| |

|

|

Projections |

|

|

Estimates |

Projections |

|

|

2009 |

2010 |

2011 |

2012 |

|

2011 |

2012 |

|

2010 |

2011 |

2012 |

|

|

|

World Output 1 |

–0.6 |

5.0 |

4.4 |

4.5 |

|

0.2 |

0.0 |

|

4.7 |

4.5 |

4.4 |

|

Advanced Economies |

–3.4 |

3.0 |

2.5 |

2.5 |

|

0.3 |

–0.1 |

|

2.9 |

2.6 |

2.5 |

| United

States |

–2.6 |

2.8 |

3.0 |

2.7 |

|

0.7 |

–0.3 |

|

2.7 |

3.2 |

2.7 |

| Euro

Area |

–4.1 |

1.8 |

1.5 |

1.7 |

|

0.0 |

–0.1 |

|

2.1 |

1.2 |

2.0 |

|

Germany |

–4.7 |

3.6 |

2.2 |

2.0 |

|

0.2 |

0.0 |

|

4.3 |

1.2 |

2.7 |

|

France |

–2.5 |

1.6 |

1.6 |

1.8 |

|

0.0 |

0.0 |

|

1.7 |

1.5 |

1.9 |

| Italy |

–5.0 |

1.0 |

1.0 |

1.3 |

|

0.0 |

–0.1 |

|

1.3 |

1.2 |

1.4 |

|

Spain |

–3.7 |

–0.2 |

0.6 |

1.5 |

|

–0.1 |

–0.3 |

|

0.4 |

0.8 |

1.9 |

| Japan |

–6.3 |

4.3 |

1.6 |

1.8 |

|

0.1 |

–0.2 |

|

3.3 |

1.4 |

2.4 |

| United

Kingdom |

–4.9 |

1.7 |

2.0 |

2.3 |

|

0.0 |

0.0 |

|

2.9 |

1.5 |

2.6 |

| Canada |

–2.5 |

2.9 |

2.3 |

2.7 |

|

–0.4 |

0.0 |

|

2.7 |

2.7 |

2.6 |

| Other

Advanced Economies |

–1.2 |

5.6 |

3.8 |

3.7 |

|

0.1 |

0.0 |

|

4.5 |

4.7 |

2.9 |

|

Newly Industrialized Asian Economies |

–0.9 |

8.2 |

4.7 |

4.3 |

|

0.2 |

–0.1 |

|

5.9 |

6.2 |

3.1 |

|

Emerging and Developing Economies

2 |

2.6 |

7.1 |

6.5 |

6.5 |

|

0.1 |

0.0 |

|

7.2 |

7.0 |

6.8 |

|

Central and Eastern Europe |

–3.6 |

4.2 |

3.6 |

4.0 |

|

0.5 |

0.2 |

|

4.3 |

3.5 |

3.9 |

|

Commonwealth of Independent States |

–6.5 |

4.2 |

4.7 |

4.6 |

|

0.1 |

–0.1 |

|

3.5 |

4.8 |

4.3 |

|

Russia |

–7.9 |

3.7 |

4.5 |

4.4 |

|

0.2 |

0.0 |

|

3.4 |

4.6 |

4.3 |

|

Excluding Russia |

–3.2 |

5.4 |

5.1 |

5.2 |

|

–0.1 |

–0.1 |

|

. . . |

. . . |

. . . |

|

Developing Asia |

7.0 |

9.3 |

8.4 |

8.4 |

|

0.0 |

0.0 |

|

9.1 |

8.6 |

8.4 |

|

China |

9.2 |

10.3 |

9.6 |

9.5 |

|

0.0 |

0.0 |

|

9.7 |

9.5 |

9.5 |

|

India |

5.7 |

9.7 |

8.4 |

8.0 |

|

0.0 |

0.0 |

|

10.3 |

7.9 |

8.0 |

|

ASEAN-5 3 |

1.7 |

6.7 |

5.5 |

5.7 |

|

0.1 |

0.1 |

|

5.1 |

6.4 |

5.2 |

| Latin

America and the Caribbean |

–1.8 |

5.9 |

4.3 |

4.1 |

|

0.3 |

–0.1 |

|

4.8 |

5.0 |

4.3 |

| Brazil |

–0.6 |

7.5 |

4.5 |

4.1 |

|

0.4 |

0.0 |

|

5.2 |

5.1 |

4.0 |

|

Mexico |

–6.1 |

5.2 |

4.2 |

4.8 |

|

0.3 |

–0.2 |

|

3.2 |

5.0 |

4.5 |

| Middle

East and North Africa |

1.8 |

3.9 |

4.6 |

4.7 |

|

–0.5 |

–0.1 |

|

. . . |

. . . |

. . . |

| Sub-Saharan

Africa |

2.8 |

5.0 |

5.5 |

5.8 |

|

0.0 |

0.1 |

|

. . . |

. . . |

. . . |

|

South Africa |

–1.7 |

2.8 |

3.4 |

3.8 |

|

–0.1 |

–0.1 |

|

3.6 |

3.4 |

4.1 |

|

Memorandum |

|

|

|

|

|

|

|

|

|

|

|

| European

Union |

–4.1 |

1.8 |

1.7 |

2.0 |

|

0.0 |

–0.1 |

|

2.5 |

1.4 |

2.2 |

| World

Growth Based on Market Exchange Rates |

–2.1 |

3.9 |

3.5 |

3.6 |

|

0.2 |

–0.1 |

|

. . . |

. . . |

. . . |

| |

|

|

|

|

|

|

|

|

|

|

|

|

World Trade Volume (goods and services) |

–10.7 |

12.0 |

7.1 |

6.8 |

|

0.1 |

0.2 |

|

. . . |

. . . |

. . . |

| Imports |

|

|

|

|

|

|

|

|

|

|

|

| Advanced

Economies |

–12.4 |

11.1 |

5.5 |

5.2 |

|

0.3 |

0.1 |

|

. . . |

. . . |

. . . |

| Emerging

and Developing Economies |

–8.0 |

13.8 |

9.3 |

9.2 |

|

–0.6 |

–0.1 |

|

. . . |

. . . |

. . . |

| Exports |

|

|

|

|

|

|

|

|

|

|

|

| Advanced

Economies |

–11.9 |

11.4 |

6.2 |

5.8 |

|

0.2 |

0.3 |

|

. . . |

. . . |

. . . |

| Emerging

and Developing Economies |

–7.5 |

12.8 |

9.2 |

8.8 |

|

0.1 |

0.2 |

|

. . . |

. . . |

. . . |

|

Commodity Prices (U.S. dollars) |

|

|

|

|

|

|

|

|

|

|

|

| Oil

4 |

–36.3 |

27.8 |

13.4 |

0.3 |

|

10.1 |

–4.1 |

|

. . . |

. . . |

. . . |

| Nonfuel

(average based on world commodity export weights) |

–18.7 |

23.0 |

11.0 |

–5.6 |

|

13.0 |

–2.4 |

|

. . . |

. . . |

. . . |

| |

|

|

|

|

|

|

|

|

|

|

|

|

Consumer Prices |

|

|

|

|

|

|

|

|

|

|

|

| Advanced

Economies |

0.1 |

1.5 |

1.6 |

1.6 |

|

0.3 |

0.1 |

|

1.5 |

1.6 |

1.6 |

| Emerging

and Developing Economies

2 |

5.2 |

6.3 |

6.0 |

4.8 |

|

0.8 |

0.3 |

|

6.5 |

4.7 |

4.4 |

|

London Interbank Offered Rate (percent)

5 |

|

|

|

|

|

|

|

|

|

|

|

| On U.S.

Dollar Deposits |

1.1 |

0.6 |

0.7 |

0.9 |

|

–0.1 |

–0.5 |

|

. . . |

. . . |

. . . |

| On Euro

Deposits |

1.2 |

0.8 |

1.2 |

1.7 |

|

0.2 |

0.4 |

|

. . . |

. . . |

. . . |

| On

Japanese Yen Deposits |

0.7 |

0.4 |

0.6 |

0.2 |

|

0.2 |

–0.2 |

|

. . . |

. . . |

. . . |

|

|

|

Note: Real effective exchange rates

are assumed to remain constant at the levels

prevailing during November 18–December 16, 2010.

Country weights used to construct aggregate growth

rates for groups of economies were revised. When

economies are not listed alphabetically, they are

ordered on the basis of economic size. The

aggregated quarterly data are seasonally adjusted. |

|

1 The

quarterly estimates and projections account for 90

percent of the world purchasing-power-parity weights. |

|

2 The

quarterly estimates and projections account for

approximately 78 percent of the emerging and

developing economies. |

|

3

Indonesia, Malaysia, Philippines, Thailand, and

Vietnam. |

|

4 Simple

average of prices of U.K. Brent, Dubai, and West

Texas Intermediate crude oil. The average price of

oil in U.S. dollars a barrel was $78.93 in 2010; the

assumed price based on futures markets is $89.50 in

2011 and $89.75 in 2012. |

|

5

Six-month rate for the United States and Japan.

Three-month rate for the Euro Area. |

The recovery is set to continue…

The baseline projections below assume that

current policy actions manage to keep the financial turmoil and

its real effects contained in the periphery of the euro area,

resulting in only a modest drag on the global recovery. This

view reflects the limited financial spillovers observed so far

across financial markets and regions, as well as the fact that

policy responses following the Greek crisis helped limit its

impact on the global recovery in the second half of 2010. The

baseline also assumes that policymakers in emerging markets

respond in a timely manner to keep overheating pressures in

check.

Activity in the advanced economies is projected

to expand by 2½ percent during 2011–12, which is still sluggish

considering the depth of the 2009 recession and insufficient to

make a significant dent in high unemployment rates. Nevertheless,

the 2011 growth projection is an upward revision of ¼ percentage

point relative to the October 2010 WEO, mostly due to a new

fiscal package passed in late 2010 in the United States that is

expected to boost economic growth this year by ½ percent. A

package with a similar growth impact passed in Japan is expected

to sustain a moderate recovery in 2011. And although growth in

the periphery of the euro area is marked down for this year,

this is offset by an upward revision to growth in Germany, due

to stronger domestic demand.

In both 2011 and 2012, growth in emerging and

developing economies is expected to remain buoyant at 6½ percent,

a modest slowdown from the 7 percent growth registered last year

and broadly unchanged from the October 2010 WEO. Developing Asia

continues to grow most rapidly, but other emerging regions are

also expected to continue their strong rebound. Notably, growth

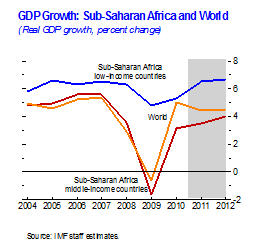

in sub-Saharan Africa—projected at 5½ percent in 2011 and 5¾

percent in 2012—is expected to exceed growth in all other

regions except developing Asia. This reflects sustained strength

in domestic demand in many of the region’s economies as well as

rising global demand for commodities (Box

1).

…and financial conditions in most regions are

expected to remain stable

Financial conditions are expected generally to

remain stable or improve this year. Bank lending conditions in

the major advanced economies are expected to ease further, and

bond issuance by nonfinancial firms is also expected to

strengthen. Amid generally sluggish recovery and continued high

saving in key emerging Asian economies, real yields are likely

to remain low through 2011. In the United States, the outlook

for Treasury yields is uncertain: a gradually strengthening

recovery and fiscal concerns may push up yields, while

quantitative easing may hold them back.

Financial stresses, however, are expected to

remain elevated in the periphery of the euro area, where market

participants are still concerned about sovereign and banking

risk, the political feasibility of current and envisioned

austerity measures, and the lack of a comprehensive solution.

European sovereign peripheral spreads and bank funding costs are

thus likely to remain elevated during the first half of this

year, and financial turbulence could re-intensify.

Under a baseline scenario in which contagion

from turmoil in the euro area periphery is contained, emerging

market capital inflows are expected to remain strong and

financial conditions robust. Bond issuance by emerging market

sovereigns and firms is expected to remain robust in 2011. Low

interest rates in mature markets and fairly strong investor

appetite will continue to pose upside risks to emerging market

flows and asset prices, despite some recent slowdown of inflows.

Box 1. Economic Outlook for

Sub-Saharan Africa

Most countries in sub-Saharan

Africa have recovered quickly from the global

financial crisis, with the region projected to grow

5½ percent in 2011. But the pace of the recovery has

varied within the region. Output growth in most oil

exporters and low-income countries (LICs) is now

close to precrisis highs. The recovery in South

Africa and its neighbors, however, has been more

subdued, reflecting the more severe impact of the

collapse in world trade and elevated unemployment

levels that are proving difficult to reduce.

Prior to the recent global crisis,

sub-Saharan Africa enjoyed a period of strong growth.

Growth in the region’s 29 LICs was particularly

impressive at more than 6 percent during 2004–08,

second only to developing Asia. This reflected the

improved political environment, favorable external

conditions, and sound macroeconomic management.

These strong initial conditions helped most

countries in the region weather the worst effects of

the food and fuel price hikes of 2007–08 and the

subsequent global financial crisis. Many countries

supported output by injecting fiscal stimulus and

lowering interest rates. As a result, LICs in the

region continued to grow at nearly 5 percent in

2009, although output fell in the region’s

middle-income countries—a grouping dominated by

South Africa. In most of the oil-exporting countries

growth slowed, with the notable exception of

Nigeria.

Most countries in the region have

now returned to precrisis growth rates. In 2011,

LICs are projected to grow by 6½ percent. Domestic

demand is being supported by automatic stabilizers,

expansion in public investment and social support

programs, and continued monetary accommodation.

Growing trade ties with Asia are also playing a role

in the region’s recovery, primarily through

commodity markets. Output growth has rebounded in

South Africa, but high unemployment and subdued

confidence are expected to continue to dampen the

pace of recovery, restricting growth to about 3½

percent in 2011.

Risks remain weighted to the

downside, however. The pace of recovery in Europe,

the dominant trade partner for most

non-oil-exporting countries in sub-Saharan Africa,

is modest and uncertain. More immediately, the sharp

pickup in fuel and food prices stands to make a

significant impact on many non-oil-exporting

countries. Rising food prices are likely to affect

the urban poor in particular, given the high share

of food in their consumption baskets. In response,

governments will need to consider targeted social

safety nets, with attendant fiscal costs. Managing

these pressures, particularly against the backdrop

of elevated fiscal deficits and narrowing output

gaps, will be an important challenge for the region

in 2011—a year with a busy political calendar,

including perhaps 17 national elections.

With recovery at hand in most

countries in the region, the emphasis of

macroeconomic policies needs to shift:

-

Countercyclical fiscal policy

helped support output growth during the crisis,

but has resulted in wider fiscal deficits across

the board. With growth in most countries now

approaching potential, the consistency of these

wider deficits with financing and medium-term

debt sustainability considerations should be

reviewed. To promote growth and poverty

reduction, attention also needs to be given to

the appropriateness of the composition of

government spending and revenue sources.

-

Inflation remains in check in

most countries, and the monetary stance seems

appropriate. But policymakers should remain

alert to potential pressure from rising

commodity prices—particularly with growth

approaching potential levels.

-

Other policy areas requiring

sustained attention include more intensive

monitoring and sounder regulation of the

financial sector, continuing policy improvements

targeted at the business environment, and robust

public financing mechanisms to plan and control

government spending, including infrastructure

investment.

|

Commodity prices will remain high, and inflation is

rising in some emerging economies

Prices for both oil and non-oil commodities rose

considerably in 2010, in response to strong global demand

but also to supply shocks for selected commodities. Upward

pressure on prices is expected to persist in 2011, due to

continued robust demand and a sluggish supply response to

tightening market conditions. As a result, the IMF’s

baseline petroleum price projection for 2011 is now $90 per

barrel, up from $79 per barrel in the October 2010 WEO. As

for non-oil commodities, weather-related crop damage was

greater than expected in late 2010, and price effects are

expected to unwind only after the 2011 crop season. As a

result, non-oil commodity prices are expected to increase by

11 percent in 2011. Near-term risks are now to the upside

for most commodity classes.

The uptick in consumer price inflation in emerging

economies in 2010 was attributable partly to rising food

prices. But the recent bout of high food price inflation has

been quite persistent, straining the budgets of low-income

households and beginning to feed into overall price

inflation in a number of economies. More important, rapid

growth in emerging and developing economies has narrowed or

in some cases closed output gaps in these economies.

Accordingly, overheating pressures are starting to

materialize in some cases. Consumer prices in these

economies are projected to rise 6 percent this year, an

upward revision of ¾ percentage point relative to the

October 2010 WEO. Signs of overheating are also becoming

apparent in some countries via rapid credit growth or rising

asset prices.

The picture is quite different in advanced economies,

where still-ample economic slack and well-anchored inflation

expectations will generally keep inflation pressures

subdued. Inflation is expected to remain at 1½ percent this

year, unchanged from 2010 and a slight upward revision from

the October 2010 WEO.

Downside risks remain elevated

Downside risks arise from the possibility of tensions in

the euro area periphery spreading to the core of Europe; the

lack of progress in formulating medium-term fiscal

consolidation plans in major advanced economies; the

continued weakness of the U.S. real estate market; high

commodity prices; and overheating and the potential for

boom-bust cycles in emerging markets. On the upside, there

are risks from stronger-than-expected business investment

rebounds in major advanced economies.

The risk of financial turmoil spreading from the

periphery to the core of Europe is a by-product of

continuing weakness among financial institutions in many of

the region’s advanced economies, and a lack of transparency

about their exposures. As a result, financial institutions

and sovereigns are closely linked, with spillovers between

the two sectors occurring in both directions. Although the

periphery accounts for only a small portion of the euro

area’s overall output and trade, substantial financial

linkages with countries in the core, as well as financial

spillovers through higher risk aversion and lower equity

prices, could generate a slowdown in growth and demand that

would hinder the global recovery. In particular, continued

market pressures could result in serious funding pressures

for major banks and sovereigns, increasing the likelihood

that problems spill over to core countries.

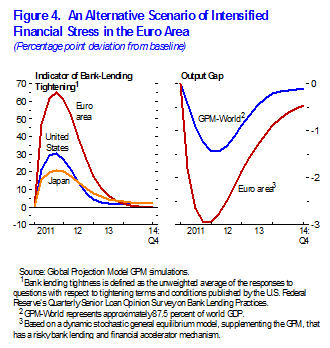

Figure 4 (CSV|PDF)

presents an alternative scenario that illustrates how larger

spillovers can subtract from growth. The scenario—which is

broadly similar to the one presented in the

July 2010 WEO Update—assumes that a large shock

followed by insufficiently rapid and strong policy action

results in significant losses on securities and credit in

the euro area periphery. This causes capital ratios to fall

substantially in several countries, both in the periphery

and the core. Under such a scenario, European banks tighten

lending conditions by a similar magnitude as during the

collapse of Lehman Brothers in 2008. As a result, euro area

growth is reduced by about 2½ percentage points relative to

the baseline. Assuming that financial spillovers to the rest

of the world are limited—with the increase in bank-lending

tightness in the United States about half that in

Europe—global growth in 2011 is lower by about 1 percentage

point than in the baseline. But if financial contagion to

the rest of the world is more severe—resulting in a spike in

generalized risk aversion, a drying up of liquidity, and

sharp falls in equity markets—the impact on global growth

would be substantially larger, amplified by balance sheet

weaknesses in other major advanced economies.

Another downside risk stems from insufficient progress in

developing medium-term fiscal consolidation plans in large

advanced economies. The recently implemented stimulus

measures in the United States and Japan make it more

challenging to ensure medium-term fiscal sustainability.

Therefore, it has become even more important to formulate

more credible plans to bring debt down over the medium term.

On the upside, business investment could rebound faster

than currently expected in key advanced economies,

underpinned by strong corporate sector profitability.

In emerging economies, key risks relate to overheating, a

rapid rise of inflation pressures, and the possibility of a

hard landing. In the near term, upside risks to growth have

risen, driven by accommodative policies, strong

terms-of-trade gains for commodity exporters, and resurgent

capital inflows. If, however, policymakers fall behind the

curve in responding to nascent overheating pressures and

asset price bubbles, macroeconomic policies in key emerging

economies could be setting the stage for boom-bust dynamics

in real estate and credit markets and, eventually, a hard

landing in these economies. With emerging markets now

accounting for almost 40 percent of global consumption and

more than two-thirds of global growth, a slowdown in these

economies would deal a serious blow to the global

recovery—and to the rebalancing that needs to take place.

Decisive policy actions are needed to lessen risks and

sustain growth

Despite the signs of near-term decoupling—between the

periphery and core of Europe, between financial stresses and

the real economy, and between advanced and emerging

economies—the global economy remains tightly interconnected.

A host of measures are needed in different countries to

reduce vulnerabilities and rebalance growth in order to

strengthen and sustain global growth in the years to come.

In the advanced economies, the most pressing needs are to

alleviate financial stress in the euro area and to push

forward with needed repairs and reforms of the financial

system as well as with medium-term fiscal consolidation.

Such growth-enhancing policies would help address

persistently high unemployment, a key challenge for these

economies. They would also produce beneficial spillovers to

emerging economies, where the main policy challenge is to

respond appropriately to capital inflows, keep overheating

pressures in check, and facilitate external rebalancing.

In the euro area, comprehensive, rapid, and decisive

policy actions are required to address downside risks.

Important steps at both the national and the euro-area-wide

level have been taken since May, including measures to

strengthen fiscal balances and introduce structural reforms,

the stepping up of extraordinary liquidity support and the

introduction of the Securities Markets Program by the

European Central Bank (ECB), and the establishment of the

temporary European Financial Stability Facility (EFSF), to

be succeeded by the permanent European Stability Mechanism (ESM)

after 2013. But additional strengthening of national policy

actions to further secure fiscal sustainability and rekindle

growth continues to be key in many countries. Markets remain

skittish about potential losses in the region’s banks and

have not been assuaged by stress tests conducted to date.

New stress tests that are more realistic, thorough, and

stringent will increase clarity. They will need to be

followed quickly by recapitalization. Markets also need to

be reassured that sufficient resources are available from

the center to deal with downside risks and that the overall

policy approach is consistent. Hence the EFSF as well as the

envisioned permanent ESM must have the ability to raise

sufficient resources and deploy them in a flexible manner,

as needed. In the meantime, the ECB will need to continue to

provide liquidity and remain active in securities purchases

to help preserve financial stability.

More generally in the advanced economies, there is a need

for continued progress to repair and reform financial

systems. This is a critical element of the normalization of

credit conditions and would help reduce the burden on

monetary and fiscal policy to support the recovery. The

specific financial sector policies needed are discussed in

more detail in the January 2011

Global Financial Stability Report Update.

The vulnerability of sovereigns emphasizes the urgency of

moving toward more sustainable fiscal paths—not just by

countries in the euro area periphery, but also by major

advanced economies. In the near term, emerging signs of a

handoff from public to private demand in many large advanced

economies suggests that countries can push forward in

formulating and implementing credible medium-term

consolidation plans. Although some targeted measures in the

United States are justifiable at this juncture given the

still weak labor and housing markets, the recently

implemented stimulus is expected to deliver only a

relatively small growth dividend (given its size) at a

considerable fiscal cost. The U.S. fiscal deficit is now

projected at 10¾ percent in 2011 (more than double that in

the euro area), and gross government debt is projected to

exceed 110 percent of GDP in 2016. The absence of a credible,

medium-term fiscal strategy would eventually drive up U.S.

interest rates, which could prove disruptive for global

financial markets and for the world economy. It is thus even

more critical that policies be put in place to bring debt

down over the medium term. Such measures could include

entitlement reforms, caps on discretionary spending, reforms

of the tax system to boost fiscal revenue, and the

establishment or strengthening of fiscal institutions.

Fiscal issues are discussed in more detail in the January

2011 Fiscal Monitor Update.

At the same time, monetary accommodation needs to

continue in the advanced economies. As long as inflation

expectations remain anchored and unemployment stays high,

this is the right policy from a domestic perspective.

Furthermore, it seems to have had an effect: following the

news in August that a second round of quantitative easing

was imminent, long-term rates fell to new lows in the United

States. Although U.S. Treasury yields have since increased,

particularly in the last quarter of 2010, this seems

primarily attributable to the improving outlook for the U.S.

economy, a fact corroborated by the strong performance of

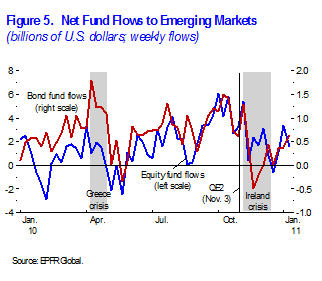

equity markets. From an external perspective, however, there

is concern that quantitative easing in the United States

could result in a flood of capital outflows toward emerging

markets. The recent slowdown in capital inflows to emerging

markets suggests that such effects may be limited so far (Figure

5:

CSV|PDF).

In contrast, monetary tightening should begin or continue

in emerging economies where overheating pressures are

starting to emerge. Recent policy rate hikes by various

countries are welcome in this regard, although in some of

them more nominal exchange rate appreciation would have been

preferable. Such tightening can, however, exacerbate the

strong capital inflows that many of these economies are now

experiencing. Therefore, prudential measures to keep

increases in credit or asset markets from becoming excessive

should also be considered.

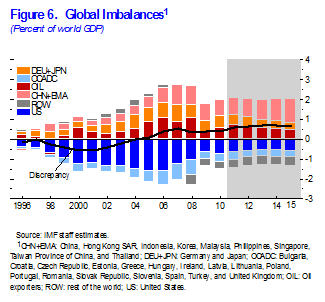

The renewed surge in capital inflows to some emerging

markets, whether driven by stronger fundamentals in the

emerging economies themselves or by looser monetary policy

in advanced economies, requires an appropriate policy

response. A number of these economies quickly overcame the

crisis and have continued to run current account surpluses (Figure

6:

CSV|PDF),

yet their real effective exchange rates remain close to

precrisis levels—that is, the response to renewed capital

inflows has been to accumulate even more foreign exchange

reserves. For these countries, allowing the currency to

appreciate would help combat overheating pressures and

facilitate a healthy rebalancing from external to domestic

demand. In other countries where the currency is above

levels consistent with medium-term fundamentals, fiscal

adjustment can help lower interest rates and restrain

domestic demand. Macroeconomic policy responses may, however,

need to be complemented by strengthened macro-prudential

measures (for example, stricter loan-to-value ratios,

funding composition restrictions) and, in some cases,

capital controls.

|

Source |