| |

|

|

|

|

|

|

|

|

|

|

|

Table 1.

Overview of the World Economic Outlook

Projections

(Percent change unless

otherwise noted) |

|

|

|

|

Year over Year |

|

|

|

|

| |

|

|

|

|

|

Difference from April 2011 WEO

Projections |

|

Q4 over Q4 |

| |

|

|

Projections |

|

|

Estimates |

Projections |

|

|

2009 |

2010 |

2011 |

2012 |

|

2011 |

2012 |

|

2010 |

2011 |

2012 |

|

|

|

World Output1 |

–0.5 |

5.1 |

4.3 |

4.5 |

|

–0.1 |

0.0 |

|

4.7 |

4.3 |

4.4 |

|

Advanced Economies |

–3.4 |

3.0 |

2.2 |

2.6 |

|

–0.2 |

0.0 |

|

2.7 |

2.3 |

2.6 |

| United

States |

–2.6 |

2.9 |

2.5 |

2.7 |

|

–0.3 |

–0.2 |

|

2.8 |

2.6 |

2.5 |

| Euro

Area |

–4.1 |

1.8 |

2.0 |

1.7 |

|

0.4 |

–0.1 |

|

2.0 |

1.8 |

2.0 |

|

Germany |

–4.7 |

3.5 |

3.2 |

2.0 |

|

0.7 |

–0.1 |

|

3.8 |

2.6 |

2.4 |

|

France |

–2.6 |

1.4 |

2.1 |

1.9 |

|

0.5 |

0.1 |

|

1.4 |

2.0 |

2.1 |

|

Italy |

–5.2 |

1.3 |

1.0 |

1.3 |

|

–0.1 |

0.0 |

|

1.5 |

1.3 |

1.2 |

|

Spain |

–3.7 |

–0.1 |

0.8 |

1.6 |

|

0.0 |

0.0 |

|

0.6 |

0.9 |

2.0 |

| Japan |

–6.3 |

4.0 |

–0.7 |

2.9 |

|

–2.1 |

0.8 |

|

2.4 |

0.8 |

2.2 |

| United

Kingdom |

–4.9 |

1.3 |

1.5 |

2.3 |

|

–0.2 |

0.0 |

|

1.5 |

2.0 |

2.4 |

| Canada |

–2.8 |

3.2 |

2.9 |

2.6 |

|

0.1 |

0.0 |

|

3.3 |

2.7 |

2.7 |

| Other

Advanced Economies2 |

–1.1 |

5.8 |

4.0 |

3.8 |

|

0.1 |

0.0 |

|

4.7 |

4.0 |

4.3 |

|

Newly Industrialized Asian Economies |

–0.7 |

8.4 |

5.1 |

4.5 |

|

0.2 |

0.0 |

|

5.9 |

5.1 |

5.3 |

|

Emerging and Developing Economies3 |

2.8 |

7.4 |

6.6 |

6.4 |

|

0.1 |

–0.1 |

|

7.5 |

6.9 |

6.6 |

| Central

and Eastern Europe |

–3.6 |

4.5 |

5.3 |

3.2 |

|

1.6 |

–0.8 |

|

4.9 |

5.1 |

2.2 |

|

Commonwealth of Independent States |

–6.4 |

4.6 |

5.1 |

4.7 |

|

0.1 |

0.0 |

|

4.5 |

5.2 |

3.6 |

|

Russia |

–7.8 |

4.0 |

4.8 |

4.5 |

|

0.0 |

0.0 |

|

4.3 |

5.3 |

3.4 |

|

Excluding Russia |

–3.0 |

6.0 |

5.6 |

5.1 |

|

0.1 |

0.0 |

|

. . . |

. . . |

. . . |

|

Developing Asia |

7.2 |

9.6 |

8.4 |

8.4 |

|

0.0 |

0.0 |

|

9.2 |

8.4 |

8.6 |

|

China |

9.2 |

10.3 |

9.6 |

9.5 |

|

0.0 |

0.0 |

|

9.8 |

9.4 |

9.5 |

|

India |

6.8 |

10.4 |

8.2 |

7.8 |

|

0.0 |

0.0 |

|

9.7 |

7.7 |

8.0 |

|

ASEAN-54 |

1.7 |

6.9 |

5.4 |

5.7 |

|

0.0 |

0.0 |

|

6.0 |

5.4 |

5.8 |

| Latin

America and the Caribbean |

–1.7 |

6.1 |

4.6 |

4.1 |

|

–0.1 |

–0.1 |

|

5.4 |

4.3 |

4.0 |

|

Brazil |

–0.6 |

7.5 |

4.1 |

3.6 |

|

–0.4 |

–0.5 |

|

5.0 |

4.3 |

3.7 |

|

Mexico |

–6.1 |

5.5 |

4.7 |

4.0 |

|

0.1 |

0.0 |

|

4.4 |

4.4 |

3.7 |

| Middle

East and North Africa |

2.5 |

4.4 |

4.2 |

4.4 |

|

0.1 |

0.2 |

|

. . . |

. . . |

. . . |

|

Sub-Saharan Africa |

2.8 |

5.1 |

5.5 |

5.9 |

|

0.0 |

0.0 |

|

. . . |

. . . |

. . . |

|

Memorandum |

|

|

|

|

|

|

|

|

|

|

|

| European

Union |

–4.1 |

1.8 |

2.0 |

2.1 |

|

0.2 |

0.0 |

|

2.1 |

1.9 |

2.3 |

| World

Growth Based on Market Exchange Rates |

–2.1 |

4.0 |

3.4 |

3.7 |

|

–0.1 |

0.0 |

|

. . . |

. . . |

. . . |

| |

|

|

|

|

|

|

|

|

|

|

|

|

World Trade Volume (goods and services) |

–10.8 |

12.4 |

8.2 |

6.7 |

|

0.8 |

–0.2 |

|

. . . |

. . . |

. . . |

| Imports |

|

|

|

|

|

|

|

|

|

|

|

|

Advanced Economies |

–12.5 |

11.6 |

6.0 |

5.1 |

|

0.2 |

–0.4 |

|

. . . |

. . . |

. . . |

|

Emerging and Developing Economies |

–7.9 |

13.7 |

12.1 |

9.0 |

|

1.9 |

–0.4 |

|

. . . |

. . . |

. . . |

| Exports |

|

|

|

|

|

|

|

|

|

|

|

|

Advanced Economies |

–12.0 |

12.3 |

6.8 |

6.1 |

|

0.0 |

0.2 |

|

. . . |

. . . |

. . . |

|

Emerging and Developing Economies |

–7.9 |

12.8 |

11.2 |

8.3 |

|

2.4 |

–0.4 |

|

. . . |

. . . |

. . . |

|

Commodity Prices (U.S. dollars) |

|

|

|

|

|

|

|

|

|

|

|

| Oil5 |

–36.3 |

27.9 |

34.5 |

–1.0 |

|

–1.1 |

–1.8 |

|

. . . |

. . . |

. . . |

| Nonfuel

(average based on world commodity export weights) |

–15.7 |

26.3 |

21.6 |

–3.3 |

|

–3.5 |

1.0 |

|

. . . |

. . . |

. . . |

| |

|

|

|

|

|

|

|

|

|

|

|

|

Consumer Prices |

|

|

|

|

|

|

|

|

|

|

|

| Advanced

Economies |

0.1 |

1.6 |

2.6 |

1.7 |

|

0.4 |

0.0 |

|

1.6 |

2.6 |

1.6 |

| Emerging

and Developing Economies3 |

5.2 |

6.1 |

6.9 |

5.6 |

|

0.0 |

0.3 |

|

6.2 |

5.8 |

5.0 |

|

London Interbank Offered Rate (percent)6 |

|

|

|

|

|

|

|

|

|

|

|

| On U.S.

Dollar Deposits |

1.1 |

0.5 |

0.6 |

0.8 |

|

0.0 |

–0.1 |

|

. . . |

. . . |

. . . |

| On Euro

Deposits |

1.2 |

0.8 |

1.7 |

2.6 |

|

0.0 |

0.0 |

|

. . . |

. . . |

. . . |

| On

Japanese Yen Deposits |

0.7 |

0.4 |

0.5 |

0.2 |

|

–0.1 |

–0.1 |

|

. . . |

. . . |

. . . |

|

|

|

Note: Real effective exchange rates

are assumed to remain constant at the levels

prevailing during April 14–May 12, 2011. When

economies are not listed alphabetically, they are

ordered on the basis of economic size. The

aggregated quarterly data are seasonally adjusted. |

|

1The

quarterly estimates and projections account for 90

percent of the world purchasing-power-parity

weights. |

|

2Excludes

the G7 and euro area countries. |

|

3The

quarterly estimates and projections account for

approximately 80 percent of the emerging and

developing economies. |

|

4Indonesia,

Malaysia, Philippines, Thailand, and Vietnam. |

|

5Simple

average of prices of U.K. Brent, Dubai, and West

Texas Intermediate crude oil. The average price of

oil in U.S. dollars a barrel was $79.03 in 2010; the

assumed price based on futures markets is $106.30 in

2011 and $105.25 in 2012. |

|

6Six-month

rate for the United States and Japan. Three-month

rate for the euro area. |

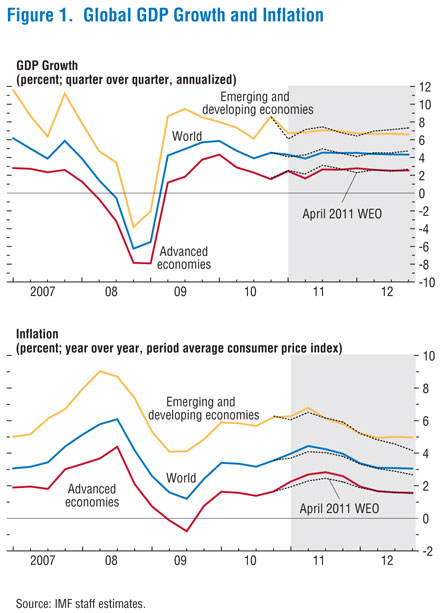

Inflation has risen

Global inflation picked up from 3½ percent in the last

quarter of 2010 to 4 percent in the first quarter of 2011, more

than ¼ percentage point higher than projected in the

April 2011 World Economic Outlook (Figure

1:

CSV|PDF,

bottom panel). Inflation accelerated mainly because of

larger-than-expected increases in commodity prices. However,

core inflation also crept up across a number of economies. Among

advanced economies, core inflation remained subdued in the

United States and Japan and rose moderately in the euro area.

Among emerging and developing economies, inflation pressures

have become increasingly broad-based, reflecting a higher share

of food and fuel in consumption as well as accelerating demand

pressure.

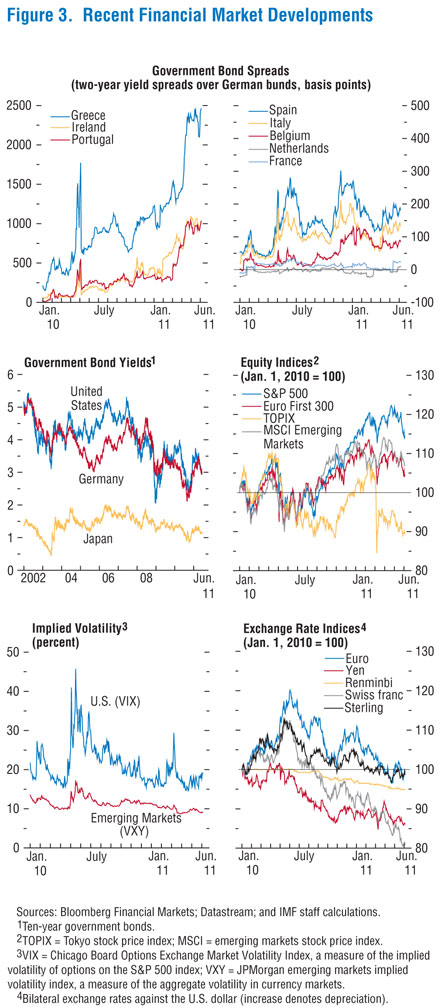

Financial volatility has increased

Financial volatility has increased

After easing through much of the first half of 2011, global

financial conditions have become more volatile since late May (Figure

3:

CSV|PDF).

This reflects market concerns about sovereign risks related to

developments in the euro area periphery and the recent softening

in activity and persistent housing market weakness observed in

the United States. Symptoms include rising sovereign credit

default swap spreads in certain euro area economies, retreating

global stock prices, and falling long-term bond yields in the

major advanced economies. In addition, the

June 2011 Global Financial Stability Report (GFSR) Market

Update emphasizes the insufficient pace of progress on

banking system repair, notably in Europe, as well as risks

related to releveraging in various market segments.

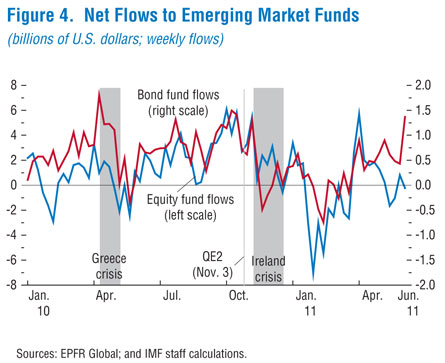

For emerging and developing economies, the financial environment

remains quite accommodative, although with greater variation

across countries. Capital inflows have been fickle (

Figure

4:

CSV|

PDF),

probably reflecting the increased downside risks to the global

economy and domestic policy concerns such as inflation. Some of

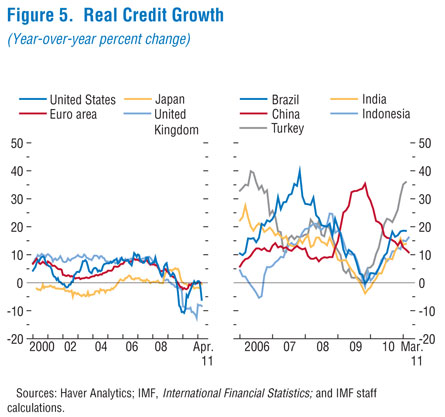

the larger economies are experiencing rapid credit growth,

propelled by accommodative macroeconomic conditions and buoyant

capital flows (

Figure

5:

CSV|

PDF).

In others, credit growth has decelerated with a persistent

tightening of monetary policy. Despite some currency gyrations (

Figure

3:

CSV|

PDF,

bottom panel), exchange rates have not moved much in real

effective terms in recent months.

Commodity prices have stabilized

Commodity markets have experienced volatility since late

April (Figure

6:

CSV|PDF).

After surging through April, commodity prices fell in May. The

corrections partly reflected the unwinding of an earlier buildup

of noncommercial derivative positions with increased general

financial volatility and in reaction to recent data on softer

global economic activity. Prices of crude oil briefly came close

to $120 a barrel in April, fell sharply in May, but have

stabilized since. Current prices average about $107 a barrel,

close to levels assumed in the

April 2011 World Economic Outlook. Food prices also

stabilized beginning in early 2011, following last year’s

weather-related supply shocks.

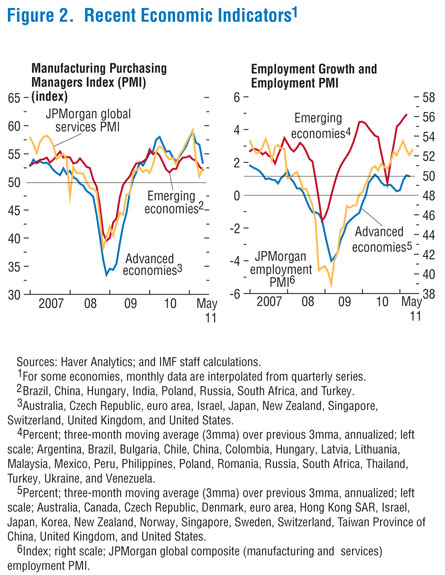

Growth will slow temporarily

Global activity is projected to slow in the second quarter of

2011, and then reaccelerate in the second half of the year. But

activity will remain unbalanced amid elevated downside risks.

Growth is set to be sluggish in advanced economies facing fiscal

and financial sector balance sheet problems, which will continue

to be a drag on employment. Activity will continue to expand

strongly in advanced economies that do not face such challenges,

as well as in many emerging and developing economies.

Forward-looking indicators such as manufacturing purchasing

managers indices suggest that activity has softened in the

second quarter of 2011, especially in many advanced economies.

The projected easing in activity comes from more subdued private

consumption, as oil price hikes in previous quarters cut into

households’ real incomes. In addition, the effect of global

supply disruptions from the Japanese earthquake is fully

materializing in the second quarter. However, the fundamental

drivers of growth remain in place: overall still-accommodative

macroeconomic conditions, pent-up demand for consumer durables

and investment, and strong potential growth in emerging and

developing economies. Accordingly, the baseline projections on

global growth and inflation remain broadly unchanged compared

with the

April 2011 World Economic Outlook (Table 1).

Growth in the advanced economies is projected to average

about 2½ percent during 2011–12, slightly weaker than in the

April 2011 World Economic Outlook. This would

represent a modest deceleration from an average of about 3

percent in 2010. For 2011, growth is expected to be weaker than

previously projected in the United States and Japan, partly

offset by stronger activity in core euro area economies. In

2012, the rebound of the Japanese economy from the earthquake is

forecast to offset weaker growth in the United States.

Output growth in emerging and developing economies is

expected to be 6½ percent during 2011–12, compared with about 7½

percent in 2010, in line with the

April 2011 World Economic Outlook projections.

Within this overall picture, prospects vary across regions.

Growth in emerging Asia will decelerate only slightly from the

very high levels of last year. Disruptions to regional

production networks due to supply constraints from Japan appear

contained, although some sectors, especially automobiles and

electronics, could experience strains through the summer. Latin

America will be bolstered by commodity exports and domestic

demand but the pace will ease in some economies where policies

have been tightening more aggressively (see

box). Growth in emerging Europe is now projected to be

higher than previously expected in 2011, followed by a softening

in 2012, driven in part by a sharp domestic demand cycle in

Turkey. Activity is projected to continue strengthening in

sub-Saharan Africa, with domestic demand remaining robust and

commodity exporters benefiting from elevated prices. Economic

prospects in the Middle East and North Africa remain clouded by

political and social unrest, although the outlook has improved

for some oil and mineral exporters.

Increasing downside risks

The balance of risks points down more than at the time of the

April 2011 World Economic Outlook. Downside risks

due to heightened potential for spillovers from further

deterioration in market confidence in the euro area periphery

have risen since April (see the

June 2011 GFSR Market Update). Market concerns

about possible setbacks to the U.S. recovery have also surfaced.

If these risks materialize, they will reverberate across the

rest of the world—possibly seriously impairing funding

conditions for banks and corporations in advanced economies and

undercutting capital flows to emerging economies. In addition,

banks in advanced economies continue to face a wall of

refinancing requirements, and a squeeze on banks’ wholesale

funding could reverse the recent normalization of lending

standards. Near-term risks for sharper or more drawn-out

negative spillovers from Japan to other economies cannot be

ruled out either.

|

Economic Outlook for Latin

America and the Caribbean

Growth remains robust in Latin

America and the Caribbean (LAC) and is projected to

exceed 4½ percent in 2011. The expansion has been

strongest in South America, where high commodity

prices and easy external financing conditions are

fueling domestic demand, which, if left unchecked,

could soon lead to overheating. The recovery in many

Central American and Caribbean countries has gained

some strength, although growth continues to be

constrained by strong real links with slower-growing

advanced economies (particularly the United States),

less favorable terms of trade, and in some cases

high public debt.

Latin America recovered quickly and

strongly from the global financial crisis. In most

countries, prudent, countercyclical policies in the

years leading up to the crisis allowed the

deployment of macroeconomic stimulus to counteract

its effects on activity. The region expanded by more

than 6 percent in 2010, led by South America, where

high commodity prices, easy external financing

conditions, and accommodative macroeconomic policies

stimulated domestic demand. Output gaps have closed

in much of the region and early signs of overheating

are appearing: inflation is rising, current account

deficits are widening, and credit and asset prices

are growing rapidly. Rising global fuel and food

prices are adding to the challenge of containing

inflation and protecting the poor.

LAC growth is projected to moderate

to about 4½ percent in 2011 and to converge to its

potential rate, about 4 percent, over the next two

years. The expansion will continue to be led by

domestic demand, and accompanied by a further

widening in the current account deficit. This

baseline scenario assumes a significant withdrawal

of policy stimulus and some deceleration of private

sector demand, particularly for large commodity

exporters. There are signs that activity is finally

gaining traction in economies with closer real links

to advanced economies, where the recovery has

lagged. However, growth in many Central American and

Caribbean countries will continue to be constrained

by the slow recovery in remittances and tourism and

less favorable terms of trade. High public debt will

require sustained fiscal consolidation in the

Caribbean, which will also pose a drag on growth.

Although downside risks persist for

the world economy, risks for the near-term outlook

in Latin America are somewhat more balanced. GDP

growth could be higher if the assumed policy

tightening does not materialize or proves

insufficient to slow domestic demand. Under this

scenario, however, inflation and current account

deficits could turn out higher than projected,

raising the risk of boom-bust dynamics. On the

downside, a serious tightening in global financial

conditions could lead to a reversal in inflows to

the region and adversely affect its prospects.

With output gaps closed in most

countries, macroeconomic policy accommodation should

be removed. Even though many countries have moved in

recent months to raise policy interest rates, it is

still critical to continue to adjust the policy mix

by reducing the pace of government spending to avoid

placing an excessive burden on monetary policy in

the context of sizable capital inflows and currency

appreciation. In light of strong credit and asset

price growth, countries should also continue to

strengthen macroprudential measures and possibly use

capital controls to enhance the resilience of their

financial systems. In Central America, emphasis must

shift to rebuilding the policy buffers used during

the global recession, while in the Caribbean, where

public debt is very high, fiscal policy will need to

continue with consolidation to ensure economic

stability and set the stage for sustainable growth

in the future.

| |

|

|

|

Selected Western

Hemisphere Economies: Real GDP1

(Annual percent

change) |

| |

|

Projections |

| |

2010 |

2011 |

2012 |

|

|

|

North America |

3.1 |

2.7 |

2.8 |

| Canada |

3.2 |

2.9 |

2.6 |

| Mexico |

5.5 |

4.7 |

4.0 |

| United

States |

2.9 |

2.5 |

2.7 |

| |

|

|

|

|

Central America, Panama, and the Dominican

Republic2 |

4.7 |

4.4 |

4.5 |

| Costa Rica |

4.2 |

4.3 |

4.4 |

| Dominican

Republic |

7.8 |

5.5 |

5.5 |

| Guatemala |

2.8 |

3.0 |

3.2 |

| Panama |

7.5 |

7.4 |

7.2 |

| |

|

|

|

|

Caribbean3 |

-1.3 |

2.7 |

3.5 |

| Eastern

Caribbean Currency Union |

-2.1 |

2.1 |

2.6 |

| Haiti |

-5.1 |

8.6 |

8.8 |

| Jamaica |

-1.2 |

1.4 |

2.4 |

| Trinidad and

Tobago |

-0.6 |

1.8 |

2.6 |

| |

|

|

|

|

South America4 |

6.6 |

4.7 |

4.1 |

| Argentina5 |

9.2 |

6.0 |

4.6 |

| Brazil |

7.5 |

4.1 |

3.6 |

| Chile |

5.2 |

6.2 |

5.0 |

| Colombia |

4.3 |

4.6 |

4.5 |

| Peru |

8.9 |

6.6 |

5.9 |

| Venezuela |

-1.5 |

3.3 |

3.9 |

| |

|

|

|

|

Latin America and the Caribbean6 |

6.1 |

4.6 |

4.1 |

|

|

|

Source: IMF, World Economic

Outlook database. |

|

1Regional

growth rates weighted by GDP valued at

purchasing power parities. Selected

countries comprise at least 70 percent of

output for each subregion. |

|

2Includes

also Belize, El Salvador, Honduras, and

Nicaragua. |

|

3Includes

also The Bahamas and Barbados. Eastern

Caribbean Currency Union includes Antigua

and Barbuda, Dominica, Grenada, St. Kitts

and Nevis, St. Lucia, and St. Vincent and

the Grenadines, and the United Kingdom

territories of Anguilla and Montserrat. |

|

4Includes

also Bolivia, Ecuador, Guyana, Paraguay,

Suriname, and Uruguay. |

|

5Private

analysts are of the view that real GDP

growth was significantly lower than the

official estimates in 2008 and 2009,

although the discrepancy between private and

official estimates of real GDP growth

narrowed in 2010. |

|

6Includes

Mexico and economies from the Caribbean,

Central America, and South America. |

|

Regarding commodities, risks are smaller than projected in

April but still point down for growth. Unrest in the Middle East

may raise oil prices. Although pressures in food markets have

eased somewhat, low inventories and weather-related supply

disruptions present significant near-term upside risk for

prices.

Fiscal challenges continue to pose various risks for the

recovery. A first set of concerns revolves around fiscal

imbalances in the euro area periphery. A second set involves the

large near-term fiscal adjustment in the United Sates against a

still-fragile recovery. A third set of concerns centers on

medium-term fiscal sustainability in the United States and

Japan. In the United States, these risks are rising because of

the absence of credible consolidation and reform plans, while

Japan’s plans must be made sufficiently ambitious and be

implemented. In Japan, the fiscal response to the earthquake has

raised challenges to attaining medium-term fiscal

sustainability. Some credit rating agencies have already put

U.S. and Japanese sovereign credit ratings on negative watch.

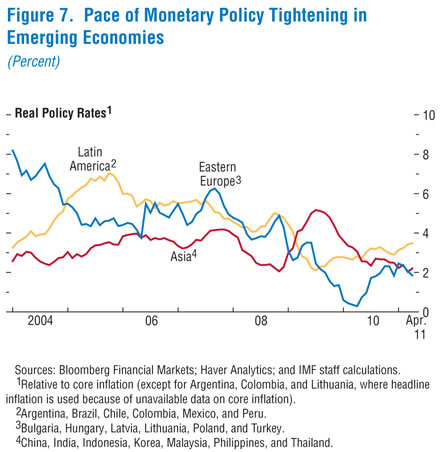

Overheating pressures in some key emerging economies have

also intensified as observed in elevated inflation pressures,

and in some cases high asset prices. While some economies have

tightened at a faster pace, others have fallen somewhat behind

the curve (Figure

7:

CSV|PDF).

The longer policy rates stay low, the larger the chances of a

hard landing in the future.

Upside risks from stronger investment by a generally healthy

corporate sector in advanced economies, or buoyant near-term

activity in emerging and developing economies, are broadly at

the same level as estimated in the

April 2011 World Economic Outlook.

Policies need to steer

away from unbalanced growth

The global economy has turned the corner from the Great

Recession. However, securing the transition from recovery to

expansion will require a concerted effort at addressing diverse

challenges.

The key fiscal priority for major advanced

economies—especially the United States and Japan—is to implement

credible and well-paced consolidation programs focused on

bolstering medium-term debt sustainability. Given the tepid

recoveries in these economies thus far, consolidation should

ideally be gradual and sustained, so as not to undermine growth

prospects. For the United States, it is critical to immediately

address the debt ceiling and launch a deficit reduction plan

that includes entitlement reform and revenue-raising tax reform.

Should the recovery threaten to turn out substantially weaker

than currently projected, the pace of fiscal adjustment should

be modified accordingly, within the envelope of a credible

medium-term consolidation plan. Similarly, Japan needs to make

progress in tax and entitlement reforms to alleviate its

worrisome debt dynamics. Further fiscal issues are discussed in

the

June 2011 Fiscal Monitor Update.

Advanced economies must also address the financial sector

vulnerabilities that were at the root of the crisis. In this

regard, the situation is more critical in various European

economies than elsewhere. In the euro area periphery, there is

no way around ambitious structural reforms to boost

competitiveness and revive employment growth, along with

front-loaded fiscal adjustment and balance sheet repair to

restore market confidence and ameliorate the pressure on

sovereign and bank spreads. These efforts need to be flanked

with concrete steps to strengthen EU-wide supervision and crisis

resolution, including by making the safety net more flexible.

In advanced economies with still-sizable economic slack and

continued drag from fiscal and financial sector consolidation,

monetary policy should stay accommodative—this includes the

United States, Japan, and the euro area. As the recovery

proceeds and economic slack diminishes more broadly, however,

central banks must guard against further increases in core

inflation. Importantly, accommodative monetary policy cannot

become a substitute for insufficient financial sector repair. In

the meantime, macroprudential policies and stronger financial

supervision can help contain risks flowing from a prolonged

period of low interest rates.

In a number of emerging and developing economies that are

already operating at or above precrisis levels of output, the

priority is to expeditiously tighten macroeconomic policies, and

use exchange rate flexibility and macroprudential tools,

possibly including capital controls, to help contain risks of

boom-bust cycles. While many emerging and developing economies

are already raising policy rates, real rates still remain low.

Thus, policy tightening must continue, coordinated with

transparent central bank communication to anchor inflation

expectations. Economies with high fiscal deficits or debt also

need to rebuild room for fiscal policy maneuver, especially

those that are susceptible to external shocks or have sharply

widening current account deficits (or currencies approaching

overvaluation ranges). At the same time, social sector spending

and priority infrastructure investment must be preserved. For

economies with excessive current account surpluses, particularly

in Asia, demand rebalancing—through exchange rate appreciation

and structural reforms—remains a top priority for securing

balanced growth and employment gains in the medium term.